Indian VCs have a secret—it’s called ‘dry powder’ and it’s just waiting to be invested. Dry powder is essentially money that’s not tied up in other investments and can be quickly deployed when the right opportunity comes along.

Rajan Anandan, the managing partner at Peak XV Partners, recently spoke about this. He sees potential for growth and innovation, and foresees India making a significant impact on the global stage.

At the Global IndiaAI Summit, Anandan said, “Our firm has over INR 16,000 crore of dry powder. We just want more people starting up in AI.” He added that Peak XV has invested in 25 AI startups so far.

Emphasising that capital availability is not a problem, Anandan mentioned that the venture capital ecosystem has $20 billion ready to be invested in Indian startups. He also noted that AI is currently the most significant theme, with investors showing strong enthusiasm for startups in this field.

Recently, Speciale Invest also hosted DevCon, with 50+ technical founders and engineering leaders. Even Stellaris Venture Partners recently hosted an AI Agents Hackathon, in a bid to attract a lot of talent in the space.

It’s only a matter of time before the $20 billion dry powder is ‘snorted’ by the AI companies of India, as every VC is slowly turning into an AI-focused investment firm.

The Mystery Behind the $20-Billion ‘Dry Powder’

This brings up the question: Where is all this money coming from?

Kyle Stanford, a senior VC analyst at PitchBook, noted that a large portion of the capital invested in high-end venture deals comes from asset managers like mutual funds, hedge funds, and private equity funds.

“A lot of recently closed VC funds have been holding onto their capital and waiting for the market to bottom out, or they have a better sense of what the pricing of these deals should be,” he said.

When it comes to India, according to data from research firm Preqin, PE/VC dry powder in India increased to $15.6 billion by March 2023, up from $12.8 billion in 2022 and $11.1 billion at the end of 2021.

Seventy India-focused PE/VC firms closed funds in 2022, raising an aggregate of $8.5 billion — the highest-ever annual fundraising value, Preqin said.

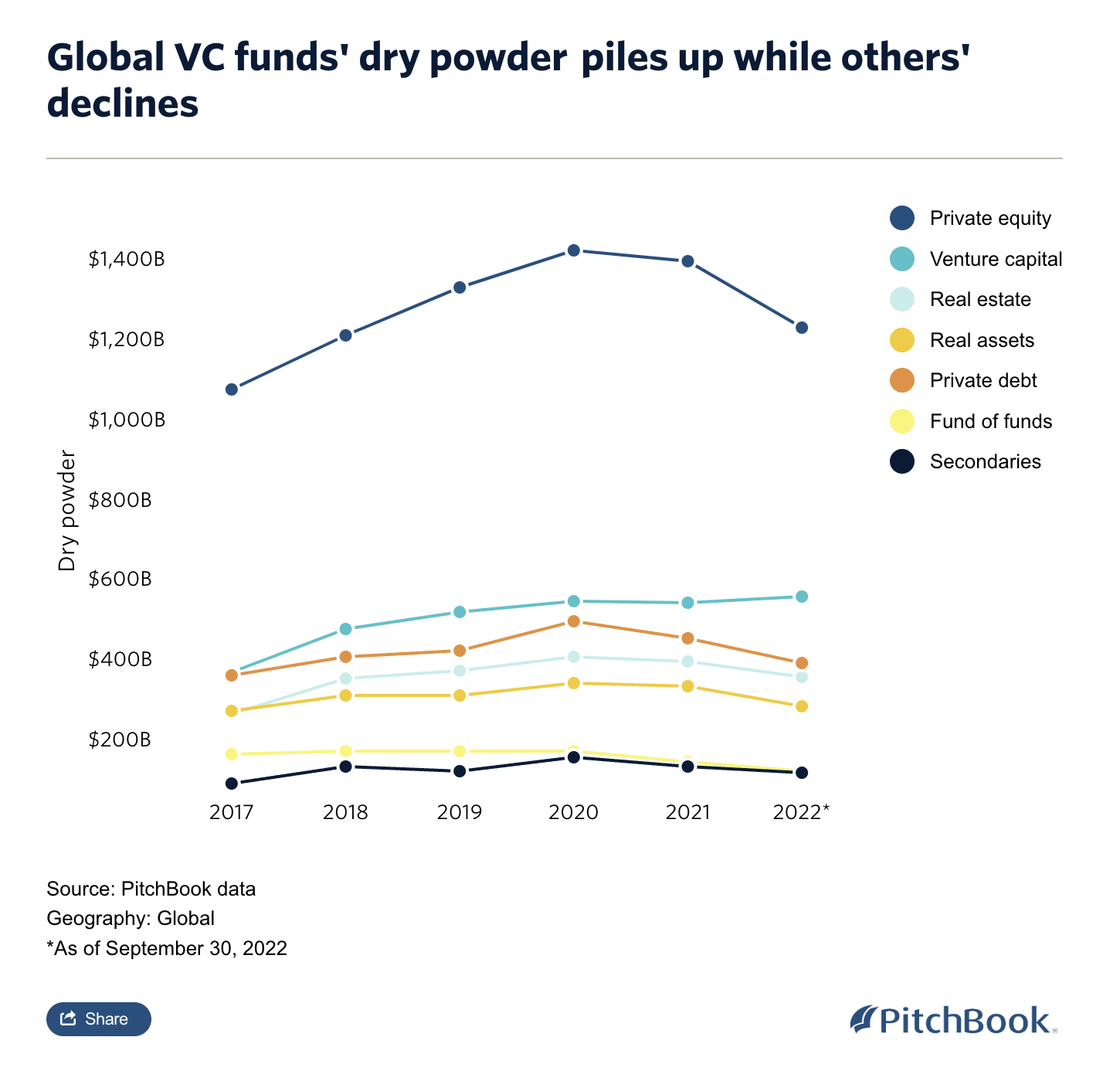

Strong fundraising in the first half of 2022 also contributed to these substantial dry powder reserves. Global venture firms amassed a total of $223.6 billion through Q3, with most of the capital coming from the first two quarters. If this pace continues, it will surpass the total capital raised in 2021, according to PitchBook data.

According to a Bain & Co report, the funding from the investors’ side has seen a significant decline since 2021, with annual funds dropping from $40 billion in 2021 to just $4 billion till June 2024.

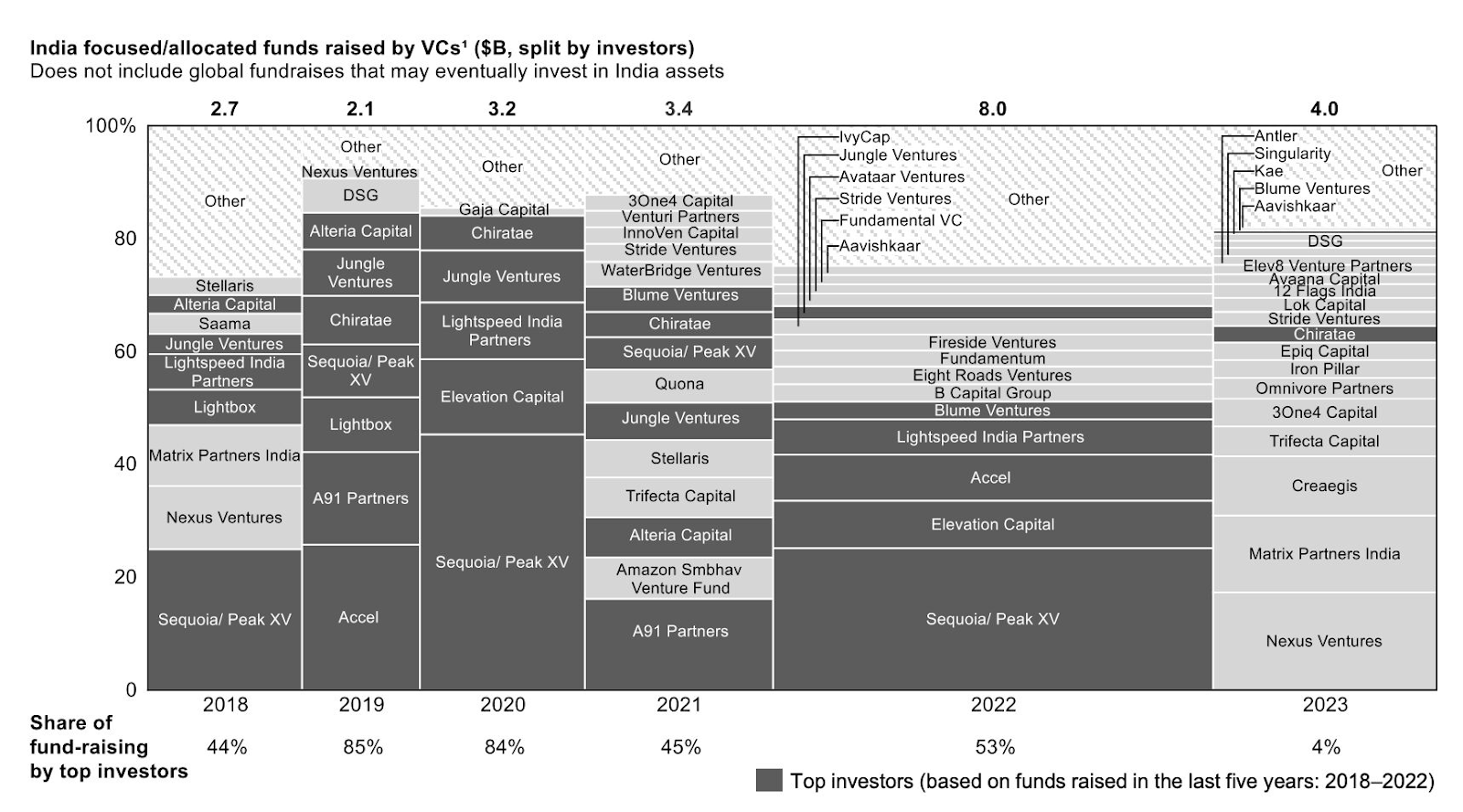

Moreover, the share of fundraising by top investors varies significantly each year, peaking at 85% in 2019 and dropping to 4% in 2023. There is a notable increase in total funds raised in 2022 compared to other years, and a significant drop in 2023.

This means that the fund accumulated in 2022 is still kept by the investors, adding the cumulative money from all the years.

Meanwhile, data from the Q3 2022 PitchBook-NVCA Venture Monitor shows that through Q3 2022, the total value of venture deals involving nontraditional investors reached $145.1 billion, representing about 74% of all US VC deals.

This group of investors participated in around 92% of mega-sized venture deals in 2021.

A key factor enabling global VCs to maintain and grow their record amounts of dry powder is the significant involvement of nontraditional VC investors.

This additional capital, which isn’t counted in the VC dry powder figures, has increased the funds available to startups and helped expand the asset class beyond what is accessible to traditional VC firms.

More Funds Needed in India

When speaking with AIM, Arjun Rao, managing partner at Speciale Invest, said that the investors can’t give funds of $10 million or more because that is around 20% of the total fund size for many.

“We probably need more funds that are of larger size. The gap is in the VC market itself and hopefully some of the homegrown funds that have started in the past 10 years are growing by them having done well in the past cohorts. Their AUM is growing and therefore they can write large checks,” said Rao.

Rao also explained that one of the reasons for such a small cycle of funds is the time horizon of their LPs. “We are sort of bound by that. It’s like, ‘Hey! I got to invest, see the company, build, and grow and then make returns and then return the capital to our investors within a meaningful time horizon’,” he added.

Many believe that Indian investors are risk averse. But that is not the case according to Anandan as Peak XV has already invested in two semiconductor companies, a space tech company, and a hydrogen recycling company, proving their risk-taking capabilities.

While the term “funding winter” has been floating around, Anandan’s optimism provides a refreshing contrast. Despite the challenges, the availability of such a substantial amount of dry powder ensures that promising ventures won’t be left out in the cold.